- Individuals & Families

- Businesses

- Agents & Brokers

- Embedded Insurance

Chubb ranked #1 for Customer Satisfaction with the Home Insurance Claims Experience

Chubb ranked #1 for Customer Satisfaction with the Home Insurance Claims Experience

Chubb ranked #1 for Customer Satisfaction with the Home Insurance Claims Experience

Chubb ranked #1 for Customer Satisfaction with the Home Insurance Claims Experience

Because pets are family, Chubb now offers pet insurance with top-rated coverage from Healthy Paws.

Chubb offers the insurance protection you need for travel’s many “what ifs”.

Chubb protects small businesses at every stage – from newly formed start-ups to long-time anchors of the community.

Stay ahead of cyber threats with our free Cyber Claims Landscape Report.

Learn more about our dedicated learning paths, Online Learning Center, and more.

Many digital-savvy consumers look for it as a core or add-on option.

Many digital-savvy consumers look for it as a core or add-on option.

Many digital-savvy consumers look for it as a core or add-on option.

Chubb’s in-house technology makes it easy to integrate what we do into your customer experience.

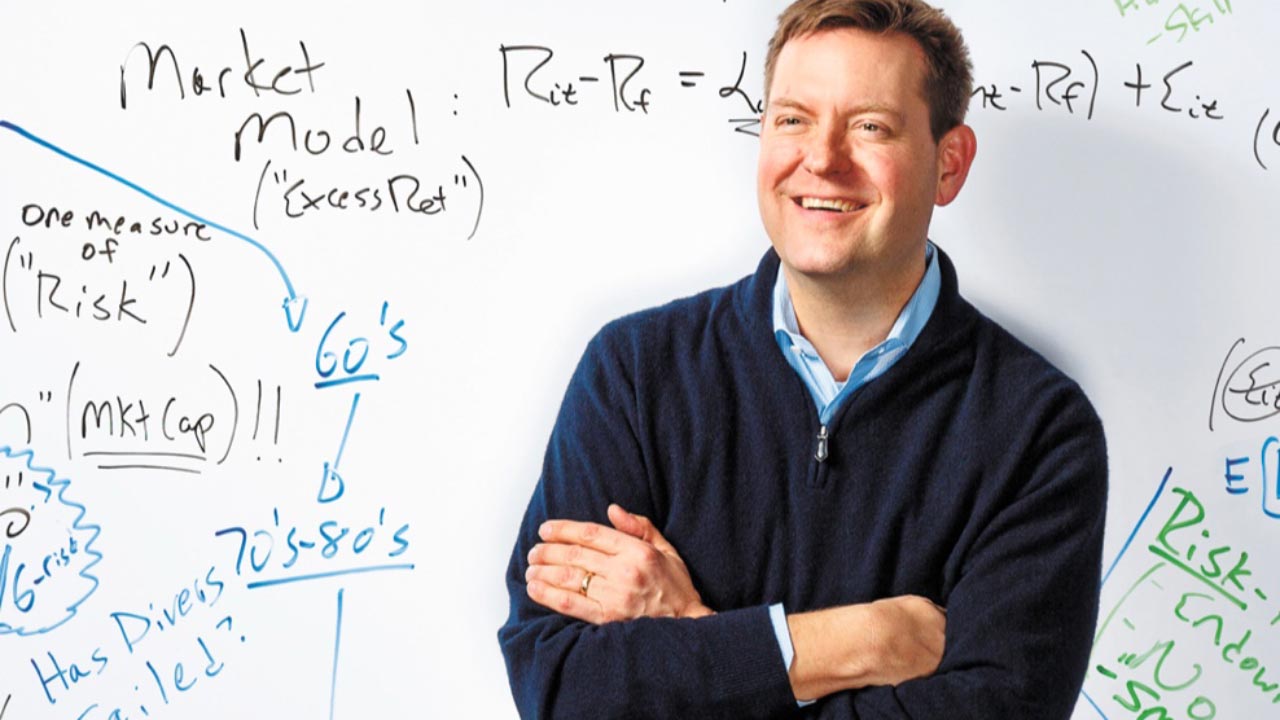

Out of Left Tail

Key insights from Wharton

Wealth advisors are familiar with the complex financial needs of ultra-high-net-worth (UHNW) individuals. But a new research report from the Wharton School of Business, commissioned by Chubb, highlights differences in how advisors and their clients evaluate assets and coordinate risk management activities. These differences are particularly true when it comes to tangible assets like property, collections, and other valuables.

The Wharton research

Partnering with an experienced property and casualty insurance agent or broker can help you close the gaps in risk management, more precisely evaluate tangible assets and risks, and incorporate risk management strategies into your clients’ balance sheets. In other words, the right insurance can better safeguard your clients’ wealth, help their portfolios achieve greater risk-adjusted returns, and protect against substantial losses from a left-tail event—an infrequent, potentially catastrophic event, such as an accident and accompanying lawsuit.

Protect your clients from left-tail events

Get the research in full or short formats so you can gain the insights to better protect and add value to your UHNW clients. Plus, understand what you should look for in an independent insurance agent or broker who can handle these types of accounts.

Explore the full study, including Wharton’s analysis of the findings.

Download the short report for an overview of the key insights.

Get the facts you need to select the right property and casualty insurance agent or broker.

How to protect your clients’ stories

Access our case studies and the key insights you need to apply Wharton’s research to your client’s portfolio.

Explore our insurance case studies to see how this type of coverage can help to preserve your clients’ wealth.

Read the applications of optimized insurance on ultra-high-net-worth individuals — and how they can help protect their assets from left-tail events.

Share our resources

Browse our video library and other resources to understand the key research findings — then share them further.

Explore the full study, including Wharton’s analysis of the findings.

Download the short report for an overview of the key insights.

Get the facts you need to select the right property and casualty insurance agent or broker.

Explore our insurance case studies to see how this type of coverage can help to preserve your clients’ wealth.

Read the applications of optimized insurance on ultra-high-net-worth individuals — and how they can help protect their assets from left-tail events.