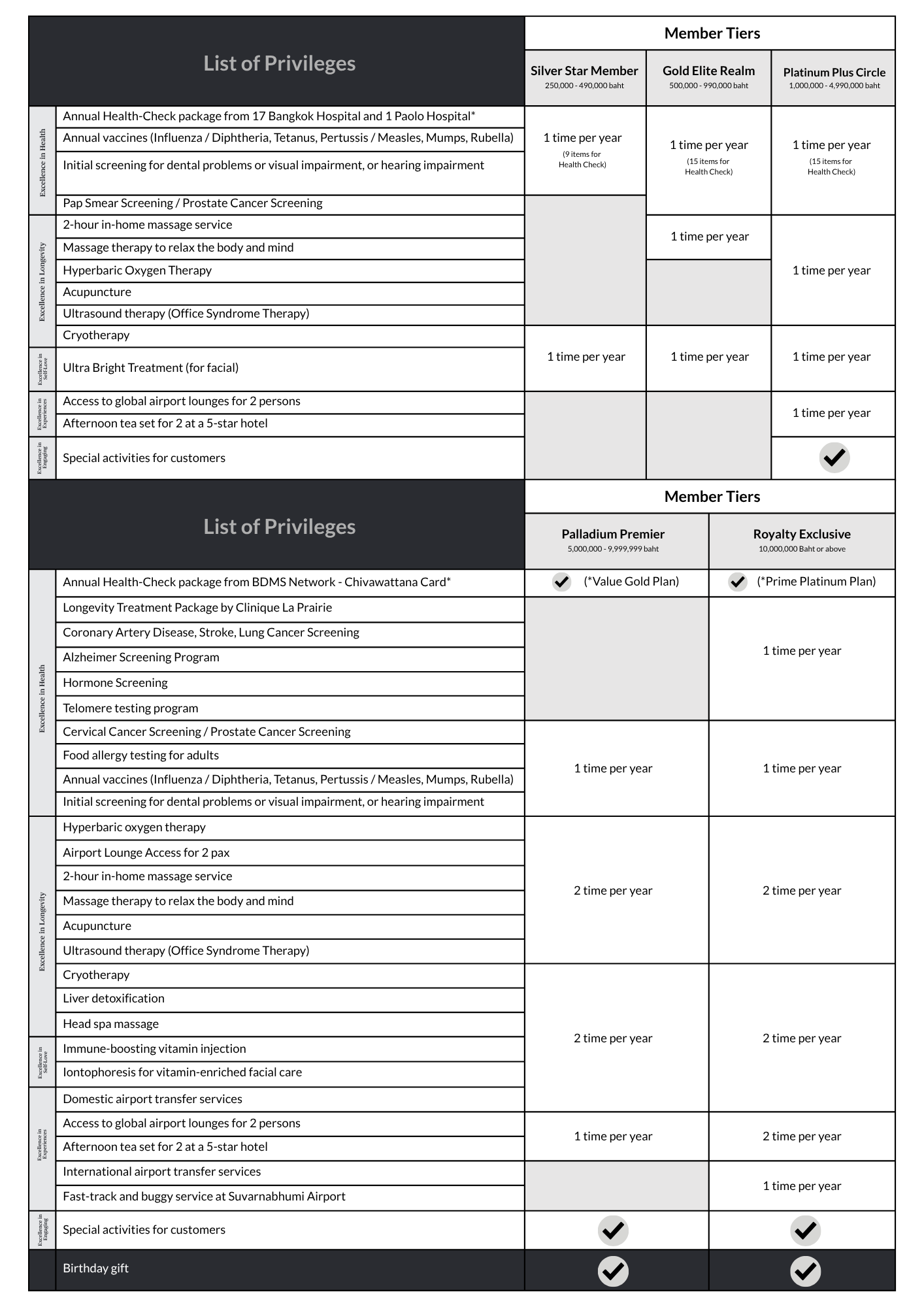

1. Eligible Insurance Products Group

Individual Life Insurance Products

- The value of 100% of the Regular Premiums from every type of ordinary life insurance policy (OL), except all plans of personal accident insurance policy and group policy, is calculated.

- The value of 120% of the premiums for all plans of riders, except Health Delight Plus (HDPN) - the medical expense and surgical fee (hospital) rider, and Health Premium Extra with Deductible (HPED) - the medical expense and surgical fee (hospital) rider, in which premiums will not be included in the calculation, is calculated.

- For the Guaranteed Insurability Option (GIO) Plan

- The value of 50% of the paid premiums for the policy approved from 1 January 2025 onwards is calculated.

- The value of 100% of the paid premiums for the policy approved before 1 January 2025 is calculated.

The GIO insurance plan requires no medical examination and questionnaires. This plan consists of Smart Savings 15/8, 678 Step Savings, Annuity Ready and Step Annuity 90/10, 90/60, etc., including other products in the GIO group offered for sale before 2025 and remained effective, and other products in the GIO group plan that the Company may offer for sale in the future.

Unit Linked Insurance Product

- The value of 120% of the Regular Protection Premium (RPP) is calculated.

- The value of 10% of the Regular Top-up Premium (RTU) and Lump Sum Top-up Premium (LSTU) is calculated.

The premium calculation excludes premiums from the following cases.

- Premiums from Smart Savings 12/4 - the endowment life insurance product

- Premiums from the products of Health Delight Plus (HDPN) - the medical expense and surgical fee (hospital) rider, and Health Premium Extra with Deductible (HPED) - the medical expense and surgical fee (hospital) rider

- Unpaid premiums from the Unit Linked plan due to a premium holiday

- Regular premiums under waiver of premium due to disability (WP)

- Regular premiums and riders under waiver of premium due to the premium payer’s death or disability (PB)

Nevertheless, total annual premium shall be calculated according to the conditions prescribed by the Company, and the Company reserves the right to revise or change the method of total annual premium calculation as deemed appropriate by the Company.

2. Only total annual premiums for all policies paid within any year are calculated.

In addition, the calculation for the member tiers will affect the entitlement of the member tier in the following year; for instance, the total annual premium amount for all policies paid within 2024 will affect the entitlement of the member tiers in 2025 onwards.

3. The Company will calculate life insurance premiums for membership tiering twice in 2025.

The details of the period for calculating the renewal premium are as follows:

| Premium Calculation | Premium Calculation Period | Cut-Off Date For Member Tier Calculation | Privilege Usage Period | | | |

| First Time | 1 January 2024 – 31 Dec 2024 | 31 December 2024 | 1 February 2025 –

30 June 2026 | | | |

| Second Time | 1 July 2024 – 30 June 2025 | 30 June 2025 | 15 July 2025 –

30 June 2026 | | | |

4. Only the member tier of the insured, as specified in the insurance policy, excluding the premium payer and policy owner, is calculated.

5. The member tier is calculated for all insurance policies held by the insured with the same Identity Card Number or Passport Number only.

6. The privilege granted cannot be transferred to any other person under any circumstances, except for a minor (an individual who is underage and below 20 full years of age, and is not legally married). The minor’s premiums will automatically be calculated for the premium payer until the minor reaches the age of 20 (for the premiums which will be calculated for the insured).

7. The member tier is not calculated for the deceased insured.

8. Only information from the date on which the Company receives the renewal premium payment is referred to, and the total annual premium calculation shall align with the conditions stipulated by the Company.

9. The policy within the premium calculation method must be the in-force policy, except in the case of Reduced Paid-Up (RPU) Insurance or Extended Term Insurance (ETI).

Remark:

The Company reserves the right to change the conditions for campaign participation and/or privileges as deemed appropriate by the Company or cancel the conditions for granting exclusive privileges without prior notice. Some items of privilege are proprietary and operated by the partner companies. The Company reserves the right to disclaim any responsibility for any changes arising from the said privileges or the operations of the partner companies.